The veteran business loan gap is real — but not in the way most veterans think. 44% of veteran business owners never apply. They assume they will be rejected. SBA data says they are wrong. Here is what the numbers show.

Carlos had a capability statement. He had a letter of intent on a federal contract. His credit score was above 700. He had two decades of active duty, a DD-214, and a service-connected disability rating. He assumed he would not qualify. He applied anyway. He was approved in eleven days. He spent the next six months wishing he had applied a year sooner.

Carlos is not unusual. The SBA says veterans are among the most creditworthy small business owners in the country. Yet they apply for loans less than almost any other group. What veterans believe about their eligibility and what is true are two different things. The SBA Office of Advocacy has published this data for years. Most veterans have never seen it.

In this post: what the 44% statistic means, who the SBA data shows gets approved, and what to do before you assume you do not qualify.

The Direct Answer: Most Veterans Who Assume They Are Not Eligible Actually Are

The SBA does not require a set age. It does not require a set credit score. It does not require years in business. Eligibility is based on your business type and your character as an owner. A veteran who assumes they do not qualify — due to a past bankruptcy, a low credit score, or a new business — is usually wrong. The SBA 7(a), SBA 504, and SBA microloans all have different rules. One of them likely fits your situation.

The 44% Problem: What the Number Actually Says

SBA data shows that roughly 44% of veteran-owned small businesses that do not apply for loans skip them out of fear of rejection. The key word is “assume.” Not “were rejected.” Not “applied and failed.” They assumed they would not qualify. So they never tried. That is the 44% problem.

This assumption costs real money. The SBA Lender Opportunity Report shows veteran-owned businesses using SBA loans survive longer than those that do not. A loan that lets you hire staff, buy gear, or bid on bigger jobs pays off over time. You cannot get that from bootstrapping alone.

Census data shows veteran-owned firms tend to work in services, construction, and government work. In those fields, capital decides who can bid. You need money for gear, bonding, and staff before you can compete. That gap is real. It is the difference between bidding on a $200,000 contract and watching someone else win it.

Who Actually Qualifies for an SBA Loan

The SBA rules may surprise you. Here is what determines whether you qualify for an SBA 7(a) loan:

- The business must be a for-profit operating in the United States or its territories

- The owner must have a genuine equity stake — not just a job offer or a contract

- The owner must have exhausted other financing options first

- Credit scores matter, but the SBA looks at character and cash flow, not just the score

- Business financials — revenue, expenses, and projections — matter more than personal assets alone

In practice: if you have been in business two years, have a credit score above 620, and can show twelve months of revenue — you have a real path to an SBA 7(a) loan. If you also have a disability rating, a business plan, and a contract in hand, your case is even stronger. These programs were built for people like you.

Why the Assumption Gap Exists

Veterans are trained to plan and avoid risk. Those are good traits in uniform. In business, they can work against you. Self-elimination costs real money.

The VA has no loan pre-check tool. It does not tell you what your credit score or revenue means for loan eligibility. The TAP briefing covers the GI Bill, disability ratings, and healthcare. It skips small business lending. That gap is built into the system.

Veterans who would qualify for an SBA loan often decide they will not — before making a single call. The 44% who skip applying because of that assumption are leaving real money on the table.

What to Do Before You Assume You Do Not Qualify

Before you decide, get a clear picture of where you actually stand. The free SEO health report we offer takes five minutes to complete. It gives you an honest read on your business’s online positioning and capital readiness signals. It is not a loan application. It is a diagnostic. Use it before you talk to a lender.

Ready to look at your options? Start with the SBA Eligibility Tool at sba.gov. It takes ten minutes. It tells you which programs you likely qualify for. If the answer is unclear, go to a Veterans Business Outreach Center. They work with you at no charge. They help you build a plan before you talk to a lender.

If you have a service-connected disability, the SBA Office of Veterans Business Development can help. VBOCs are available across the country. A counselor will help you build a plan before you talk to a bank. That prep work means walking in ready — not blind.

The Veteran Business Owner Who Applied Anyway

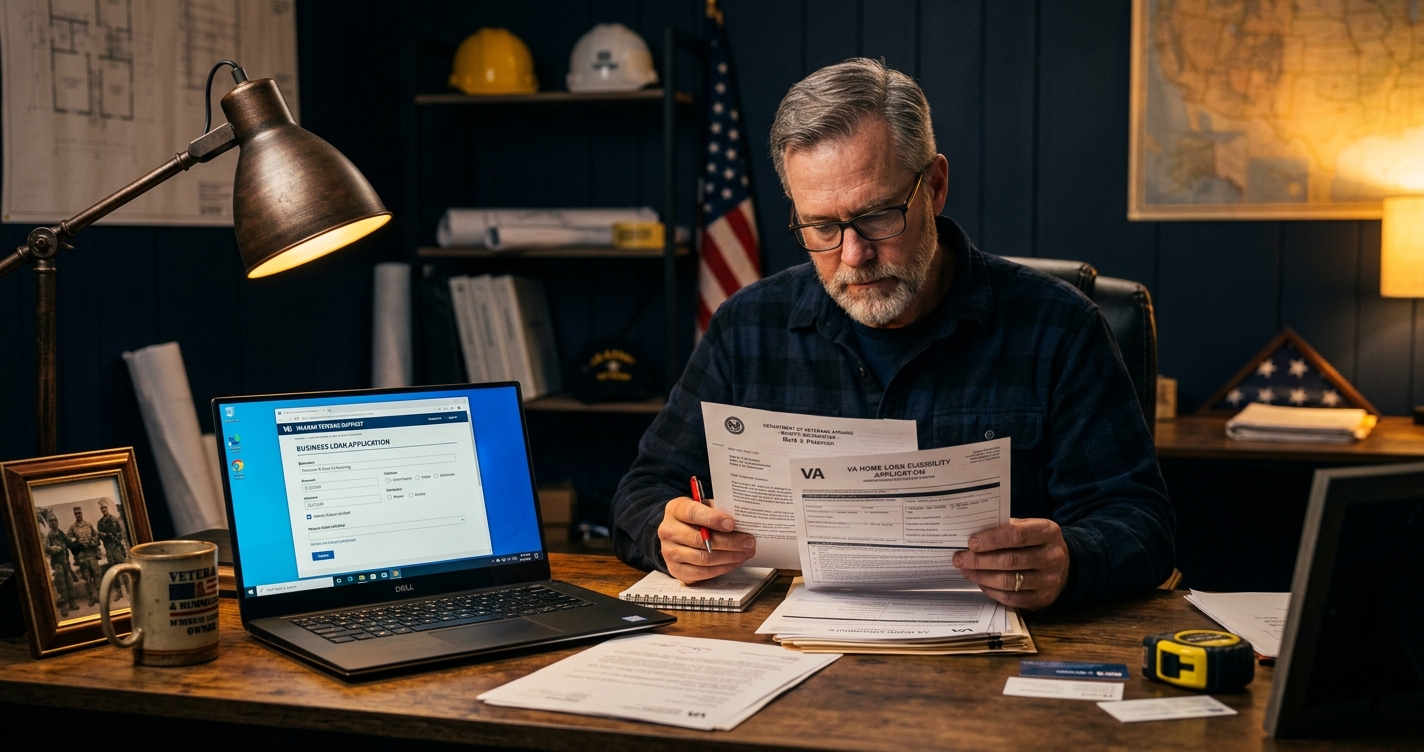

Marcus runs a logistics consulting firm in Savannah. He is a veteran. He did not think he would qualify for an SBA loan. He had a collections item on his credit report — a medical debt from three years back. His business had run for eighteen months on word-of-mouth. He assumed that collections item had closed the door.

A VBOC counselor changed the picture. The counselor explained that the SBA 7(a) program does not disqualify applicants for old medical collections. It matters that the business revenue is clean and that payments have been on time since. Marcus applied with the counselor’s help. He was approved for $75,000. That money let him hire his first two employees and buy the gear he needed to bid on a federal contract he had been watching for two years. He won that contract eight months later. His revenue tripled within eighteen months of the loan closing.

The collections item was still on his report when he applied. It did not matter. He had the right facts before he applied — not after assuming the worst.

Stop Assuming. Start Here.

If you have been running your business without capital because you assumed rejection — that assumption needs a second look. The SBA was built for this. The first step is not a loan application. It is a conversation with someone who can look at your real numbers and tell you where you stand.

The process is simpler than most veterans expect. You do not need perfect credit. You do not need years of business history. You need a business plan, twelve months of revenue history, and a clear picture of what the loan will be used for. That is the standard package for an SBA 7(a) application. If you have those three things, you have something a lender can work with. If you do not, the VBOC counselors will help you build them before you apply.

Not sure if your business qualifies? Write to us at [email protected]. We reply to every veteran inquiry within one business day. Or request your free SEO and business health report. It takes five minutes. It shows you where your business actually stands before you spend another year leaving money on the table.

What to Expect After You Apply

Most veteran business owners who complete their first SBA application are surprised by how simple the process actually is. The fear was bigger than the paperwork.

A standard SBA 7(a) application takes two to four weeks to process at most lenders. The steps are: submit the application, provide supporting documents, go through underwriting, receive a decision. If approved, funds arrive in your account within 30 days of closing.

The documents you will need: twelve months of bank statements, your most recent two years of tax returns, a one-page business summary, and your DD-214. If you have a service-connected disability rating, have that certificate ready — it opens SDVOSB-specific loan programs with lower fees and higher guaranty rates.

You do not need a lawyer. You do not need to hire a consultant to apply. The VBOC walks you through every step at no charge.

The Bottom Line

Most veteran business owners who skip loan applications do so out of habit. They assume the answer is no. They never check. The data says they are wrong. Approval rates are higher than most people think. The key is knowing where to look. Start with the SBA. Start with a lender who knows veteran programs. The first step is a simple eligibility check. That is it. One step.